It will fluctuate.

That’s the response iconic businessman and banker J.P. Morgan once gave to a reporter who asked the money mogul what the stock market will do.

Brilliant prediction!

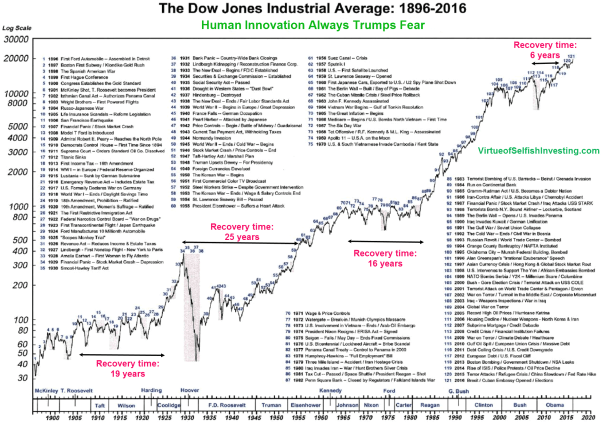

If the market has done anything since Morgan coined the famous quote, it has fluctuated. While the actual date of his quote is unknown, we know that he died in 1913 – 16 years ahead of Black Tuesday (October 24, 1929) and subsequent market crash that spawned the Great Depression. Nearly 25 years would pass before the market would return to pre-1929 levels.

Market Fluctuation as Represented by the Dow Jones Average

While no period of stock market fluctuation has been as devastating to so many Americans as the Crash of 1929, we have seen several periods of significant fluctuation since.

This is why any advisor worth his or her pay would rarely recommend that a client put all of their investment dollars in the stock market. A crash can happen at any time with little or no notice. In our lifetime, we need only look to 1987, 2000 and 2008 for examples of how people can lose a good chunk of their life savings in the stock market virtually overnight.

Why would anybody invest in the stock market if it’s so risky?

Over the long haul, the market can reward those who take on the risk with handsome returns. If you look at the last hundred years or so, stocks have provided average annualized returns of around 10%.

Buy low, sell high. Dips can mean opportunities. Big drops in the market can really chip away at your nest egg, if you have most or all of it in stocks. But they also give smart investors a shot at scoring some nice gains. Notice in the chart above how some of the sharpest rises in the Dow come after big drops. People who invested in the market shortly after the crashes made profits well before the market “recovered.” The spread from the bottom of a downturn to the top of an upturn can result in impressive returns.

Maybe you’ve heard the phrase “buy low, sell high.” That’s exactly what we’re talking about here. I know it seems unreasonable to invest in something that looks like it’s losing money, but this is a tactic many successful investors have learned. It may help you to think of stocks being sold at a discount – similar to items that go on sale the day after Christmas. They’re the same thing they were the day before; just cheaper due to lower demand.

Two ways to take advantage of a falling stock market:

- Keep some reserves in cash. If you have some money on the sidelines that is not subject to market risk, you can take advantage of dips in the market and “buy low.”

- Dollar cost average. The idea behind this approach is to invest a consistent amount on a routine basis. You’re already doing this if you have money deducted from your pay and put into your 401(k). (Assuming some of that money is invested in stocks.) Sometimes you’re buying at high prices, other times at low prices. In the end, it averages out and you reduce the risk buying high and selling low.

Diversify to help reduce risk. Spread your investments out across different types of investments – not just different stocks. Suppose you take $10,000 and buy $1,000 worth of stock in ten different companies. When a broad stock market correction (or crash) happens, you are as likely to lose money by owning ten stocks as you would if you only owned stock of one company. But if you have some of your money in other types of investments, you may lose less or even gain money when the stock market is falling.

Examples of other places to invest your money include bonds, and real estate and cash (or cashable equivalent such as a money market). It’s not uncommon for these other types of assets to stay level or go up when stocks are going down.

Types of investments (from most risky to least risky):

- Stocks, stock mutual funds, stock ETFs

- Real estate, Real Estate Investment Trusts (REIT)

- Bonds, bond funds, bond ETFs

- Cash or money market

ETF stands for exchange traded fund – a fund that is traded on the market like stocks.

Some investment pros might insist on reordering the first two bullets in the list above. I wouldn’t push back strongly. The risk with those types investments can vary greatly with different interest rate environments and economic cycles. How much you should to have in each type of investment varies for each individual.

Key questions to consider for your diversification strategy:

- What is your objective or goal for the money?

- When will you need to use the money?

- How comfortable are you with risk (i.e. day to day or week to week fluctuations)?

Your answers to these three questions should help determine what portion of your money goes into stocks, bonds and money markets. Generally speaking, the longer your time frame or the higher your risk tolerance, the more you should have in stocks and bonds. It’s also helpful to consider your money to be in different buckets. You might have a retirement bucket, a vacation fund bucket and an emergency fund bucket. Chances are you’ll want to take less risk with the money in your emergency bucket than the retirement bucket.

What should I do right now?

If all this makes sense and you know how to deal with fluctuating markets, maybe you should consider starting your own finance blog. 🙂 But there’s no reason to panic if this is over your head. Sign up to follow me right now. In future posts I’ll do my best to help you make better sense of it all in future posts.

My aim is that by the time we’re ready to retire, you’ll know enough to be able to chart your course for a comfortable lifestyle that you can afford.

Have questions? Ask them in the comment box below and I’ll address them the best I can. (Do not include personal details or dollar amounts.)