If you like to follow the performance of your mutual funds on a routine basis, you may notice that your fund values drop noticeably from time to time; sometimes even when the market moves upward. It’s very likely what you’re experiencing is a distribution of capital gains and/or dividends to shareholders.

This may be a little confusing at first because the notion of getting a distribution sounds like it would boost your fund value, not chip away at it. A mutual fund distribution works differently than a dividend paid out by a stock, which is more like a bonus for owning shares as of a particular date. The reality is that, all things being equal, you experience no change in wealth due to a mutual fund distribution.

Primer on mutual fund pricing

The fund price is technically a net asset value, or NAV for short. The daily NAV is a function of the value of all assets owned by the fund, net of the fund’s operating expenses. It’s calculated once every day that the stock market operates. If dividends are paid by securities (i.e. company stock) owned by the mutual fund, it can temporarily inflate the NAV. The same is true if a fund manager sells securities owned by the fund for more than they originally paid for it. These transactions happen daily for most mutual funds.

Why mutual fund prices drop when they pay a distribution

Every so often – usually quarterly or annually – the fund is required to pass on those distributions to anyone who owns mutual fund shares on the “record date”. When distributions are paid out, the NAV is reduced by the amount of the distribution. If you’ve elected to reinvest your distribution amounts, you’ll get a proportionately new number of shares on the same day the price drops. The net result is no change in your account value.

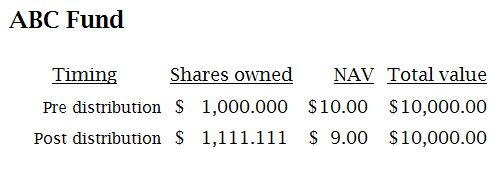

Mutual fund distribution example:

- Let’s say you own 1,000 shares of the ABC Mutual Fund. The fund has a net asset value (NAV) of $10 per share. Your investment in the fund equals $10,000.

- The total value of your holding in the fund is $10,000 (1,000 shares at $10 per share) and you reinvest all capital gains and dividends.

- The fund distributes long-term capital gains as described in the previous example.

- The long-term capital gain upon the sale of stock in the previous example is 10% of the fund’s total net asset value or $1 per share.

- Shareholders of record on the record date will receive $1 for each share they own and the NAV of the fund will be reduced by $1 on the ex-dividend date.

- As a result, you receive $1,000, which is automatically reinvested in the fund.

- Assuming no change in the market value, you still own $10,000 of the fund.

How? The fund’s NAV was reduced to $9 by the capital gains distribution of $1 and you reinvested the gain to give you a total of 1,111.11 shares ($1,000 reinvested in at the new NAV of $9 buys 111.11 shares). If you did not reinvest the gain, you would have 1,000 shares at $9 and $1,000 cash. Either way, you have $10,000.

Types of mutual fund distributions

- Dividends

- Long-term capital gains

- Short-term capital gains

Timing of mutual funds distributions

Although some funds pay distributions on a quarterly basis, it’s more likely to happen in December. Not all funds pay distributions and some funds may pay distributions one year, but not the next. The longer the gap between distributions, the larger the distribution is likely to be. If you’re curious about the distribution track record of a fund you are interested in, you can usually find distribution history online by looking up the fund name or ticker symbol.

What to do if your mutual fund pays a distribution

Your mutual fund manager will handle the entire transaction on your behalf. If your distribution is taxable, they will send you a Form 1099-Div in January of the year following the distribution. Your main responsibility is to make sure that distribution is reported on your tax return.

Ways to reduce impact of mutual fund distributions

Since mutual fund distributions can result in higher taxes, you may wish to reduce or avoid them. Here are a few tactics some people use:

- Bypass the distribution. If you’re mutual fund shopping near year end, it’s smart to find out what the distribution record date is and invest after that date. This can help you avoid a taxable distribution for an investment that you haven’t earned any returns from.

- Look for funds with low turnover ratios. Low turnover means that the fund tends to buy and hold securities longer, resulting in fewer capital gains to distribute. Index funds and other passively-managed funds generally have relatively low turnover.

- Use tax-advantaged accounts. If you invest in mutual funds through a tax advantaged account, such as a workplace retirement plan, IRA or Roth IRA, the distributions won’t affect you at tax time.

The takeaway

When your mutual fund(s) distribute capital gains and/or dividends, you’ll experience no real gain or loss. If you notice a drop in your mutual fund’s share price, do not be alarmed. This is just an accounting exercise mutual funds are required by law to conduct. Double-check the total number of shares and your account value. Unfortunately, you may have to pay taxes on the distribution if you own the mutual funds outside of your employer’s retirement account or IRA.

Important: The information provided here is for educational purposes and should not be considered advice. Before you make any final decisions, consult a trustworthy financial professional and/or tax planner.