Living requires money. If you’re like many of us, one of the concerns you may have is whether you’ll have enough money to live on in retirement. The good news is you can make projections now as to how much income you can expect when you hit retirement age, then take steps to help fill any income gaps you might face.

Note: This is the second post in a series called Ten things to do ten years before retirement. In other posts I’ll dig into other ways to prepare for retirement, such as making sure you’ll have more money in retirement by investing smarter and getting rid of debt.

If you read this entire post from top to bottom, you’ll learn how to:

- Estimate your retirement income from Social Security and pension(s)

- Calculate your future income shortfall (if any) based on your current income and estimated income from Social Security and pension(s)

- Determine how much you need to save in order to close your potential future income gap

Estimate your Social Security retirement income

If you’ve been blessed to spend your working years in the United States, then you’ll be able to count on Social Security for some of your income. Want to know how much? You can get a good estimate based on your personal situation at socialsecurity.gov.

- Go to the Retirement Estimator on ssa.gov.

- Read How the Retirement Estimator Works and Who Can Use the Retirement Estimator.

- Click “Estimate Your Retirement Benefits” button.

- Complete the required fields accurately. (Remember: Garbage in = garbage out.)

- Click “Next” to view your estimate.

Following is a preview of the online form you’ll complete in order to obtain your Social Security income estimate:

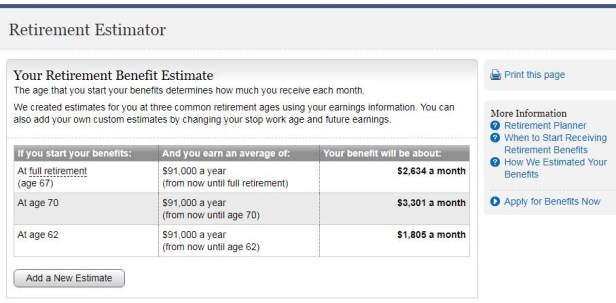

Here’s what the Social Security income estimator will tell you

The estimator shows your estimated future income if you begin taking income at these ages:

- age 67 – also known as full retirement age

- age 70 – the latest you can postpone retirement benefits

- age 62 – the earliest you can possibly begin retirement benefits

If you haven’t run your estimate already, do it now. It’s an important look into your future.

Great job! Now you have an idea how much Social Security income you can count on during your retirement years. That wasn’t so hard now, was it?

The fun is just beginning. See that “Add a new estimate” button? Click it and add another scenario.

Try this:

- See how your Social Security income would change if you increase (or decrease) your income between now and retirement.

- Play around with different income amounts and different retirement ages.

- Repeat with as many different scenarios as you wish.

Notice how the tool adds the results of all scenarios to the results page? How cool is that!

Tip: After you’ve run all the possible scenarios you’d like to consider, print the results page or take a screen shot and save to your device.

Before you leave the site completely, try running the numbers for your spouse or partner, especially if you’ll share living expenses in retirement. Keep those numbers handy because they’ll come in handy for a simple worksheet below.

Expecting a pension? Get a retirement income projection

If you work(ed) for an employer that will provide you pension income in retirement, check with the plan administrator to see how much monthly income you can expect to receive when you retire. Keep that number handy to complete the worksheet below.

Consider how your future income estimates fit into your overall retirement income picture

You may be asking yourself: How will I be able to live on that amount? Take a breath and relax. Very few people can live on their Social Security income alone.

We need to accept the reality that Social Security and pensions will only cover a portion of our expenses in retirement.

We need to accept the reality that Social Security and pensions (if you’re lucky enough to have one) will only cover a portion of our expenses in retirement. But how much? Here’s one quick way to estimate it using the 80% rule of thumb that says you’ll need about 80% of your current income in retirement.

Tip: The worksheet below to help you keep all these numbers straight.

Do this next:

- Estimate that you’ll need 80% of your current annual income in retirement. (Example: if you currently earn $50,000, calculate $50,000 x .80 = $40,000)

- Divide that figure by twelve to get the monthly amount (Example: $ 40,000/12 = $3,333)

- Subtract your estimated Social Security monthly income from your projected future need (Example: If your Social Security income estimate is $2,000 then the calculation is $3,333 – $2,000 = $1,333)

- This is your shortfall or gap, meaning you’ll need to find other ways to make up for the extra $1,333 of estimated future expenses.

Extra credit: Apply the 4% withdrawal rate rule to figure out much you’ll need in savings

Background: Scholars have figured out that if you have a sum of money, you can withdraw money at a rate of 4% per year and it will likely last you the rest of your lifetime.

For this step, we need to figure out your annual expect income shortfall.

- Take the monthly shortage you estimated above ($1,333 in our example) and multiply it by twelve (1,333 x 12 = $15,996).

- Now, divide that number by 4% (15,996 / 0.04 = $399,900).

What does this tell you?

- If a person currently lives on an income of $50,000 per year, they’ll probably need something like $40,000 a year ($3,333 per month) in retirement.

- If they estimate their Social Security income will cover about $2,000/mo. ($24,000) of their retirement expenses, they’ll have an annual shortfall of $15,966 ($1,333/mo) to fill from other sources.

- In order to have enough income to maintain their current standard of living after retiring, this person should planning on building their retirement savings balance to roughly $400,000 before they retire.

Retirement Income and Savings Target Worksheet

Complete the fields below

A) __________________ Your current salary

B) __________________ Estimated retirement income need (A x 0.8)

C) __________________ Monthly retirement income need (B ÷ 12)

D) __________________ Estimated monthly Social Security income (from SSA.gov)

E) __________________ Estimated monthly pension income (if any)

F) __________________ Monthly shortfall (C − D − E)

G) __________________ Annual shortfall (F × 12)

H) __________________ Retirement Savings Target (F ÷ 0.04)

You can use the figure in (H) Retirement Savings Target as a goal for your retirement savings and investing plan. In other words, try to build up your retirement savings to (H) before you retire.

There are more precise tools you can find on the web to help you more accurately calculate your retirement income needs and how to save for them. However, this simple exercise can help you get a sense for what you need to be working toward.

If your retirement savings target feels manageable, hurray for you! It means you’ve probably done a good job of preparing for retirement already.

If your retirement savings targets seems out of reach, don’t give up hope. There are steps you can take to help close the gap. Start by clicking the Yes button at right (or below on smartphone or tablet) to get smarter about retirement.

The takeaway

Social Security is not intended to provide for all of your income in retirement. Even if retirement is more than ten years away, it’s good to get a preview of your future income situation now and start figuring out roughly how much retirement savings you’ll need. By assessing the situation now, you can use the remaining time you have to pay off expenses and build a retirement nest egg.

Make sure to follow RetireGenX to find out what the other nine things are. Know someone else who needs this? Share this post with them.

Thankks for the post

LikeLike