If you like to play it safe with your retirement savings, you could be taking on more risk than you know.

Some of us have learned the hard way that we can lose money quickly by investing in the stock market. Others have tried investing in bonds thinking they’re safer than stocks and still lost money.

As a result, people who don’t want to lose any of their retirement savings sometimes park their money in relatively safe investments, like money markets or CDs. They’re okay with seeing only small increases in their account value, just so long as they don’t lose money. The safe route may sound like a good way to go for someone who doesn’t like to lose money, but there’s a hidden risk in doing so. It’s called inflation.

The safe route may sound like a good way to go for someone who doesn’t like to lose money, but there’s a hidden risk in doing so. It’s called inflation.

What’s the real risk of inflation?

We all know that when there’s inflation, the cost of things to go up over time. But, if you look at it another way, what inflation really does is reduce the value of the money that you currently have.

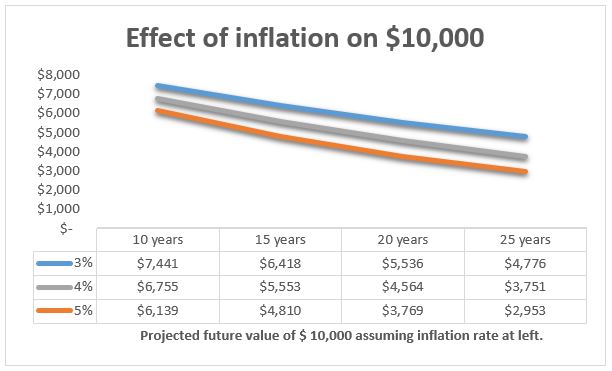

Example: If the inflation rate averaged 3% per year over a ten year period, the same $10,000 that you may have put into savings ten years ago (earning no interest) would only buy you only $7,441 worth of stuff today.

Since many of us spend 30 to 40 years working and saving, then another 20 to 30 years in retirement, even a low inflation rate can take a big bite out of your retirement savings over time. The chart below shows how inflation erodes the purchasing power of $10,000 over a number of years.

Chart A: How inflation decreases the value of money

Data source: rl360.com

Data source: rl360.com

What can I do to protect my investments from inflation?

The U.S. has been in historically low times of inflation since the year 2000, hovering mostly in the 1% to 3% range. However, we only need to look back to the 1980s and 1990s to be reminded that inflation can reach 10% per year or more.

So what can we do to protect our savings from the effects of inflation? One solution is to invest in things that provide higher return rates than the inflation rate.

In financial planning circles, advisors use the phrase real rate of return to describe what your actual total return is, after netting out the effect of inflation.

Example of real rate of return: If your investments provide a 5% return, and the inflation rate is 3%, your real return is more like 2% – but actually less (1.94%) if you use the formula used by the economists who have figured all this stuff out.

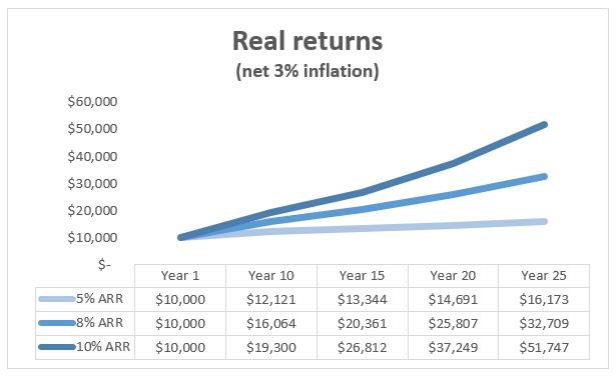

Let’s see what happens when money is invested at various rates of return over time. The chart below shows the real return of investments earning 5%, 8% or 10% – net of assumed 3% inflation – over a number of years.

Chart B: Investing can help your money grow, even when there’s inflation

Data source: Bankrate.com return on investment calculator

Conclusions:

- Chart A shows how your money can lose value over time due to the effects of inflation.

- Chart B shows that if you invest your money, you can give it an opportunity to be worth more in the future.

- Chart B also shows that the higher the investment return you earn, the more your money can grow over time.

Did you notice in Chart B how inflation has virtually no negative impact on the invested amount when returns are 5% or more? If this chart did not factor out inflation, the lines would rise even steeper.

Are investment returns of 5% or more even possible?

If you wonder whether 5% returns are even possible, chances are you’ve had some bad experiences with investing. Successful investors know that saving, patience and diversification are key.

Three keys to successful investing:

- Saving – actually put money into an account

- Patience – wait for things to improve

- Diversification – spread your investing dollars across different types of assets

The #1 key to success is actually saving money. That means putting money into your investing account. One of the best ways to do that is signing up for your retirement plan, such as a 401(k) at work. If you don’t have access to a retirement plan, look into an IRA or Roth IRA. These types of accounts are a smart way to invest for retirement because they can save you a lot of money on taxes. If you are ineligible for any of these types of investing accounts, a standard brokerage account may be your best option.

Patience is a virtue of successful investors. People that have made a lot of money with their investments have learned to sit tight when the markets get a little bumpy. On the flip side, people who pull out of the market when things start to look gloomy often lock in losses and miss out on upswings.

One phrase I learned early on that helps me remain level-headed in times of uncertainty is this: It’s time in the market – not timing the market – that will improve your results. Try to remember that simple phrase if you ever feel like you need to bail out of the market due to temporary gyrations.

Diversification is another way of saying don’t put all your eggs in one basket. What are the “baskets” in the investing world? It could refer to a particular company’s stock or type of mutual fund. Example: if you work for XYZ Corporation and they allow you to buy shares of stock through payroll deduction, it’s okay to buy some but be sure to invest in other things too. Why? If the company performs poorly financially, you could really be punished as an investor. Likewise, if you buy a mutual fund that has growth as the objective, the chances are you’ll indirectly own stake in many companies who’s stock that are likely to rise and fall in tandem with the stock market. You can diversify by putting some money into a mutual fund with the objective of generating income that will likely invest primarily in bonds.

If you want see a good case study on this topic, do a web search on what happened to Enron employees in the early 2000s. Short version: A lot of people lost their life savings overnight by being too heavily invested in Enron stock.

Thankfully, it’s easier than ever to diversify in several types of asset classes with mutual funds and ETFs (exchange-traded funds). They diversify invested dollars across many companies, but it’s still up to you to spread your money out over a number of funds (or ETFs) that invest in different asset classes, such as equities (stocks), fixed income (bonds), real estate and cash equivalents (money markets).

In recent years, money managers have introduced a new breed of funds, often referred to as lifecycle or target date funds, that help make diversification even easier. How they work is they invest proportionately higher amounts of the fund’s money in higher risk investments (such as stocks) early on and shift to more conservative investments (like bonds) over time. In theory, you can choose one fund that diversifies your money for you, and helps you get good returns over time while not “putting all your eggs in one basket.” My research on these types of funds is that they deliver good results for people who put their money in and leave it. If you go this route, be sure to find out what the fees are to make sure you’re not paying too much.

The image below from a large fund manager’s website shows how lifecycle funds are generally structured.

Notice that the longer the time frame, the more risky investments the funds hold. What’s not shown here is that the “risky” slices of the pie get smaller as we get closer to the “target date”.

Sample portfolio average annual returns over the last 25 years*

| Annual average return over 25 year period (1993 – 2017) | |

| Conservative (40% stocks, 60% bonds) | 6.92% |

| Moderate (60% stocks, 40% bonds) | 7.53% |

| Growth (80% stocks, 20% bonds) | 7.98% |

| *Data from portfoliovisualizer.com |

*Source: portfoliovisualizer.com

Whether you use a lifecycle or target date type of fund, or come up with your own mix of investments, it’s important to diversify in a few different asset classes. Numerous studies by scholars have shown that doing so can not only reduce risk, but it can also improve your returns over time.

The takeaway

Bottom line: Inflation is a real risk that all investors must contend with, as it can really chip away at the value of your money over time. Putting all your money in the stock market may seem like a simple way to beat inflation, but that approach presents its own risks. Successful investors have learned to be diligent about putting money into their investment accounts and being patient through market volatility. Want smoother ups and downs with your investments? Try diversifying across multiple asset types, either on your own by investing in a lifecycle or target date fund that does it for you.

I was always taught as a kid that the best thing to do with your money was put it in the bank. Of course, in those days interest rates beat inflation. Now, keeping your money in the bank is a sure way to lose money! Great topic, and I enjoyed seeing the way you laid out the argument against detrimental safety!

LikeLiked by 1 person